Looking to 2026 and beyond for Royal London Equity Release

Megan Williams

Marketing ConsultantShare

Looking to 2026 and beyond for Royal London Equity Release

Megan Williams

Marketing ConsultantShare

Hi Alan, great to be talking through some important topics today.

My first question is, what emerging customer behaviours or demographic shifts do you think will reshape the market by 2030?

The biggest shift is well documented - the transition from defined benefit pensions to defined contribution (DC). Many customers haven’t had long enough to build large DC pots through autoenrollment, yet homeownership remains high, creating a generational need to release property wealth to fund the required standard of living in retirement. The need is building and the equity release market must be ready, which could be a "sweet spot" opportunity for financial advisers. Various factors need to align, including interest rates, regulation, adviser adoption, customer understanding and industry capacity. As each of these click into place, the market will accelerate significantly, and we’re preparing now so we can scale smoothly when that happens.

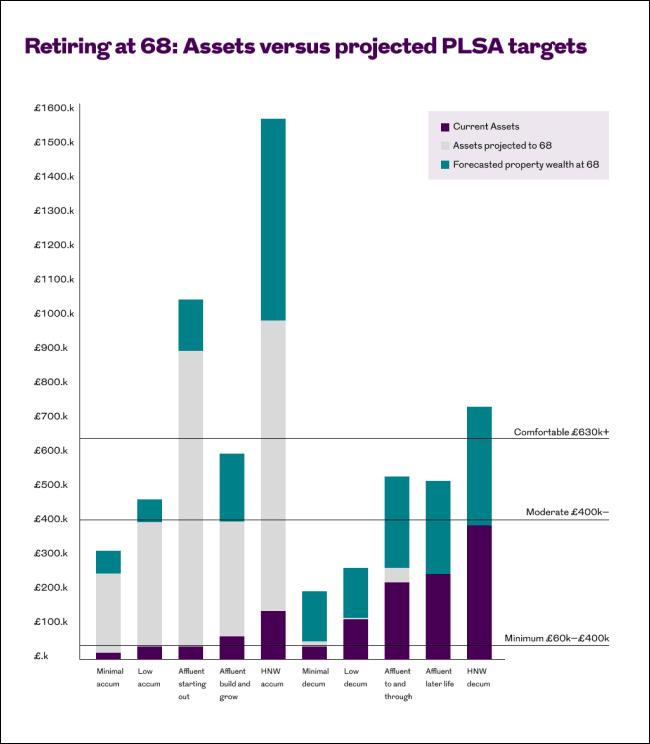

The graph below shows the impact that property wealth is projected to have on the standard of living that UK customers reach in retirement, across segments based on age and starting wealth.

How does Royal London collaborate with trade bodies and regulators to ensure property wealth becomes a standard consideration in retirement planning?

So, in my opinion, this is one of the most important areas for the equity release market. Today the market is still relatively small compared to customer need, and that need is growing all the time. We’re focused on removing barriers that stop the market from meeting the customer need.

While some factors, like the interest rate environment, are outside our control, there is a lot we can support or influence. That includes how the market is regulated, how advisers integrate equity release into holistic retirement planning, and how mortgage advisers consider equity release as a viable option for clients who need to repay a mortgage but can’t make interest payments.

It’s a priority for us to help the FCA with their market review, and we are working closely with the Equity Release Council to open up the market so that supply better meets future demand.

How does Royal London’s mutual status give you a competitive edge?

Being a mutual means that we can take a long-term view, focusing on what’s right for customers, not just on short-term shareholder returns. There’s a clear customer and adviser need for later-life lending, so we’re not waiting until the market is larger. We’re investing so that customers have strong solutions now, and so that we have scalability for when the market grows.

Royal London focused on improving adviser experience and product range in 2025. What other differentiators will Royal London Equity Release focus on in 2026?

In 2025, we strengthened the adviser experience, and we also made the Royal London-funded Principal proposition a more competitive option in the market, with product developments that included the introduction of a drawdown facility. Along with the Core product range, this gives us two strong propositions that can adapt well as the market shifts.

In 2026, our focus is on continuing to help grow the market, invest in scalability, develop propositions to enhance market share, and to make continual enhancements to stand out on customer outcomes.

We will support advisers, both those who already specialise in equity release and those who want to incorporate property wealth into planning directly, or who wish to set up referrals with equity release specialists. Helping to facilitate those mutually beneficial partnerships is key for market growth.

We’ve assessed our business architecture and processes to prioritise the areas that will have the biggest impact on scalability of service quality. We’re shaping our change capability to work in an agile way and partnering with technology providers to ensure they can support our pace of change. All of this prepares us for the wave of new business we expect as the market grows.

Royal London Equity Release is now fully integrated into the Royal London Group. What future opportunities does this unlock?

Royal London has always aimed to support advisers, helping them grow their businesses and add value for clients. Property wealth is increasingly essential in holistic financial advice, especially in retirement. With our knowledge and expert support teams, combined with Royal London’s broader capability across pensions, protection and investments, we can help advisers to expand in this space and provide more value to their clients. A great example was our recent IHT presentation by Robert Betts, Corporate & Estates Planning Specialist, at the Later Life Conference. This showcased the value of combining solutions to better meet customer needs.

Royal London Equity Release is continuing to invest in AI and operational resilience. How will these improvements support better customer outcomes?

At the moment, we’re really pleased with what we already deliver on strong customer outcomes. We have solid measurement, a mutual ethos, and teams who genuinely care about our customers.

As the market grows, however, we need to deliver that at scale. AI, automation and process improvement will help us to focus our people on the moments that truly add value, rather than on tasks that can be automated. We also expect this to support faster adviser and customer experiences, for example, in property underwriting.

How will Royal London measure good outcomes, and what indicators matter most?

We recently reviewed and refined our customer outcome metrics after learning from our first full cycle of Consumer Duty reporting. We use a layered system. Level 1 metrics are the critical measures we monitor constantly, and level 2, 3 and 4 metrics are supporting and early warning indicators.

Our level 1 metrics include, for example:

- The speed at which customers can access drawdowns

- Success at identifying and appropriately supporting vulnerable customers

- Whether customers genuinely understand the information we provide

These help us ensure quality, identify issues early and act quickly. We also benefit from Royal London’s wider capabilities and investment - for example, in enhancing solutions to support vulnerable customers.

Thanks Alan. My final question - in your opinion, what will define success for Royal London Equity Release in 2026?

The focus broadly is on making tangible progress across our four strategic pillars:

- Growing the market and seeing momentum in influencing that growth

- Increasing market share and meeting more customer needs

- Advancing scalability, tackling our highest use journeys first

- Consistently delivering strong customer outcomes, acting fast on any areas where we spot room for improvement

If we achieve those things, I’ll consider 2026 a strong year.

Sounds like an exciting year for Royal London Equity Release!

Ready to find out more?

We are exclusive providers of the Royal London Equity Release product range. All of our products are designed with your needs in mind.

Learn More